Celsius froze withdrawals in June 2022 before filing for Chapter 11 in July 2022, and Genesis froze redemptions after FTX’s collapse and filed for bankruptcy in January 2023, owing approximately $3.4 billion to its 50 largest creditors.

BlockFi, Celsius, Genesis, and Voyager together accounted for 40% of the crypto lending market and 82% of CeFi lending at their peaks, per Galaxy data. The 2022 unwind exposed two failures simultaneously: bad loans and the complete opacity of where risk sat inside those balance sheets.

The answer crypto landed on was to put lending on-chain, which helped address some of the opacity problem.

Building the credit infrastructure that institutional lenders require, such as defined seniority, first-loss retention, enforceable custody arrangements, independent administration, borrower servicing, and legal-grade bankruptcy isolation, demanded a different approach entirely.

Maple and Kraken’s warehouse facility is a test of whether DeFi can deliver that infrastructure at the collateral layer, using liquid BTC and ETH as the asset base.

Credit modelWhat it solvedWhat it left exposedWhy it matters2021–2022 CeFi lendingEasy access to yield and borrowingOpaque balance sheets, unclear risk location, weak customer visibilityCelsius, Genesis, BlockFi and Voyager exposed the failure modeAutomated DeFi lendingTransparent collateral and liquidation rulesLimited servicing, workout, legal recovery and borrower monitoringAave/Morpho-style pools are transparent but narrowRWA private creditReal-world yield brought onchainRecovery still depends on offchain legal processesGoldfinch/Lend East showed visibility does not equal recoveryMaple/Kraken warehouse facilityDefined roles, seniority, custody, first-loss capital and onchain reportingStill exposed to BTC/ETH collateral volatility and execution riskTests whether DeFi can run institutional credit infrastructure

What the structure does

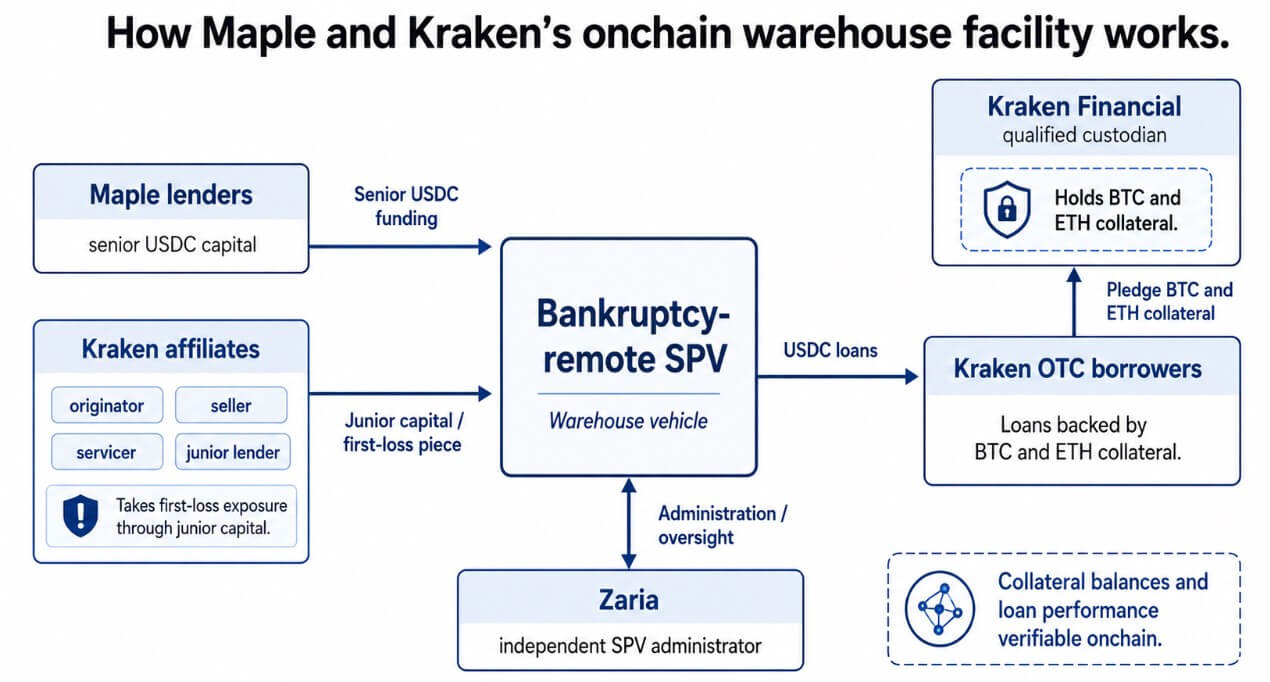

Kraken funds its OTC lending book through the USDC facility, with Maple lenders providing senior capital and Kraken affiliates originating, selling, and servicing the loans while retaining junior exposure, meaning Kraken absorbs losses before senior lenders take any hit.

Kraken Financial, a Wyoming-chartered SPDI and regulated qualified custodian, holds the BTC and ETH collateral, and Zaria administers the SPV independently.

Kraken structured the facility within a bankruptcy-remote SPV to isolate it from Kraken’s entity risk and says that collateral balances and loan performance are verifiable on-chain in real time.

Aave liquidates borrowers when the health factor falls below 1, and Morpho when LTV exceeds the market’s defined threshold, both collateral-ratio and liquidation engines, transparent and automated but bounded by what automated liquidation can handle.

Origination, servicing, monitoring, workout, and credit recovery require human judgment, legal relationships, and institutional structure that automated protocols leave unaddressed.

Maple and Kraken are adding those layers, along with legal structuring that goes beyond what smart contracts alone can enforce.

Kraken’s most forward-looking announcement line is “repeatable template for additional originators,” framing the facility as a credit infrastructure template open to other originators.

If that claim holds, the structure becomes a model for exchanges, custodians, and OTC desks seeking to grow their lending books by bringing in senior outside capital.

The problem Goldfinch identified

In April 2024, a Goldfinch governance update said Lend East expected to repay approximately $4.25 million of a $10.15 million pool, a roughly 58% principal loss, with the chain logging the loss in real time while Warbler Labs turned to external counsel and off-chain legal processes to pursue recovery.

Maple and Kraken aim to sidestep that specific failure mode by using liquid BTC and ETH as collateral, with execution on a crypto exchange taking seconds, recovering a defaulted trade-finance receivable in an emerging market takes years.

The collateral choice concentrates risk in market liquidity and execution speed, a test the structure can run quickly against observable data.

The structural bet is that crypto-native collateral pairs best with warehouse finance, with defined roles, defined seniority, and defined triggers, and a borrower underwriting layer on top.

RWA.xyz shows tokenized credit at $5.73 billion in distributed value as of June 25, with Maple as the largest platform by value at approximately $1.4 billion and a 24.6% market share. These figures show that real institutional capital is already allocated to the category.

Warehouse finance as credit infrastructure

Galaxy’s latest leverage report put total crypto-collateralized lending at $67.42 billion at the end of the first quarter, down 5.1% quarter over quarter and 14.3% below the high registered in the third quarter of 2025.

DeFi lending apps still held $28.22 billion in outstanding loans, down 13.82% in the first quarter, while CeFi lenders had $25.43 billion in open borrows, down 7.23% on the quarter.

Combining DeFi apps and CeFi lending venues, Galaxy tracked $53.65 billion of outstanding crypto-collateralized borrows at quarter-end, with DeFi’s share narrowing to 52.6% from 54.3% in the last quarter of 2025.

Galaxy said DeFi open borrows had already fallen to $23.29 billion as of May 1, down 50.58% from their Sept. 19, 2025, all-time high of $47.13 billion, following exploits and capital flight that hit on-chain lending.

That makes Maple and Kraken’s facilities more relevant to institutional credit returns, but it requires answers on collateral custody, first-loss protection, servicing, liquidation triggers, legal isolation, and what lenders can verify before stress hits.

Warehouse lines in traditional credit are the bridge between loan origination and scaled capital markets.

A World Bank/IFC document describes them as revolving facilities used to build loan portfolios for future securitization, with assets pledged to an SPV and core risk mitigants including servicing, trust agreements, custodians, overcollateralization, and legal enforceability.

SIFMA reported $232.3 billion in US ABS issuance through May 2026, up 12.6% year over year, the scale standardized structured credit reaches when its infrastructure is trusted.

Market / metricData pointArticle implicationTotal crypto-collateralized lending$67.42B in Q1 2026Crypto credit is large enough to need institutional infrastructureDeFi lending app loans$28.22B in Q1 2026Onchain lending remains significant, but volatileCeFi open borrows$25.43B in Q1 2026Centralized lending is rebuilding, but needs trust structuresDeFi open borrows by May 1$23.29BCapital flight after exploits shows transparent pools are not enoughDeFi decline from Sept. 2025 ATH-50.58%The sector still lacks durable institutional confidenceTokenized credit distributed value$5.73BInstitutional capital is already entering structured onchain creditMaple tokenized-credit value~$1.4BMaple is already a major player in the categoryMaple tokenized-credit share24.6%Shows why this facility matters beyond one dealUS ABS issuance through May 2026$232.3BTraditional structured credit shows the scale possible with trusted infrastructure

If Maple and Kraken perform through normal market volatility, the template becomes available to other originators.

Standardized LTV bands, collateral eligibility rules, liquidation triggers, custody arrangements, servicing obligations, and on-chain reporting templates could follow, creating the consistent credit documentation that institutional capital needs to allocate at scale.

Where the structure gets tested

The risk has moved from opaque balance sheets to execution, including accurate pricing during collateral declines, timely margin calls, liquid markets for liquidation, responsive custody, and servicer performance when it counts most.

If BTC or ETH gaps lower faster than margin calls execute, the facility depends on auction depth and execution speed, and multiple lenders liquidating similar collateral simultaneously can amplify selling.

That is the same forced-liquidation dynamic that crypto markets have experienced repeatedly during sharp drawdowns.

Legal structure reduces opacity, while collateral price volatility stays in the market regardless of how the credit stack is structured.

The model proves itself during a sharp BTC or ETH price drop, a liquidity gap in collateral markets, a borrower default, a servicer impairment, or a legal test of the SPV’s bankruptcy remoteness.

Coinbase offers USDC borrowing against BTC collateral through Morpho, with liquidation triggered at 86% of the BTC collateral’s market value.

Maple and Kraken build the institutional layers above that model, and each layer adds an operational dependency that requires performance during a rapid collateral decline.

What comes next

Warehouse facilities in traditional credit typically precede securitization, and originators use them to accumulate loan pools, build performance history, and standardize documentation before accessing broader capital markets.

If Maple and Kraken’s loans perform through a full market cycle, the next step could be larger pools of crypto-backed credit financed by institutional investors who need that performance record before they can allocate.

If this template spreads, crypto credit could develop consistent underwriting criteria: which collateral qualifies, at what LTV, with what liquidation triggers, held by what type of custodian, serviced under what obligations, reported in what on-chain format.

That consistency enabled the traditional ABS market to reach $232 billion in annual issuance, allowing buyers to underwrite a structure once and apply that framework across the entire loan pool.

Crypto-backed credit needs that same infrastructure layer before institutional capital allocates to it at scale, with Maple and Kraken running the first test of whether DeFi can build it.